Forex Signals Brief November 14: Traders Focused on EU Q3 GDP and US PPI Today

Yesterday the US CPI inflation highlighted the day, while today the focus will shift to the US PPI inflation and Eurozone GDP for Q3.

As expected, the U.S. CPI data showed a headline increase of 0.2% and a core measure rise of 0.3% month-over-month. Year-over-year, these figures grew by 2.6% and 3.3%, respectively. Initially, the dollar weakened but then rebounded and started to gain strength. Last night, EUR/USD closed near 1.0560, marking its lowest level for the year. On the fundamental front, several Federal Reserve officials spoke today with a hawkish tone, noting a higher neutral rate, which further supported demand for the USD.

Despite the continued strength in U.S. economic activity, Dallas Fed President Lorie Logan emphasized that the Fed should ease rates cautiously to avoid rekindling inflation. Musalem’s comments also suggested a balanced approach, pointing to the economy’s resilience and the Fed’s progress on price stability, while still recognizing inflationary pressures.

Finally, Kansas City Fed President Jeffrey Schmid highlighted the uncertainty around how much rates may fall and where they will ultimately settle.

Today’s Market Expectations

Today started with the employment report from Australia which was released early in the morning. Although there was a little gain in employment, the October employment report fell short of projections, adding fewer jobs than expected. A modest decline in the participation rate indicates a slight softening of labor market engagement, even if the unemployment rate remained stable at 4.1%. On the other hand, the underemployment rate decreased and the number of hours worked per month increased, indicating that people who are employed are putting in more hours, which could somewhat compensate for the slower job growth. In contrast to prior months, this report shows a largely stable labor market with indications of declining momentum.

The Eurozone Q3 GDP report will be released shortly, with the headline GDP figure expected to remain at 0.4%, showing a steady economic expansion with the second quarter. However a lower figure would worsen the picture for the euro further, sending EUR/USD to 1.05. We also have the employment figures, with unemployment change also expected to remain steady at 0.2%

The month-over-month (M/M) Producer Price Index (PPI) is expected at 0.2%, up from the previous 0.0%, while the annual (Y/Y) US PPI is forecasted to increase to 2.3% from 1.8%. Meanwhile, the core PPI, which excludes more volatile items, is expected to show a M/M rise of 0.3% compared to 0.2% before, with the core Y/Y figure anticipated at 3.0%, up from the previous 2.8%.

This PPI release will likely be assessed alongside yesterday’s US CPI report, which showed an October increase. If PPI comes in higher than expected, the USD may see additional gains, intensifying inflation worries. The US Unemployment Claims numbers will be released at the same time as well. While initial claims have remained within the 200K–260K range since 2022, continuing claims recently reached cycle highs, impacted by distortions from hurricane and strike activity.

Yesterday the volatility picked up during the US session, so there was enough price action for us to pull many forex trades. We opened five trading signals in total, with four of them being winning forex signals by the end of the day and just one trade closed in red. We remained long on the US Dollar and stocks, which proved to be a good trading strategy since the USD kept pushing higher, and ended up with four winning trades.

Gold Decline Stretches Further

Gold, after climbing over 50% from its November 2022 low of $1,600, has continued its bullish run through 2024, but recent weeks have shown a pullback. The weekly chart’s doji candlestick indicates a potential bearish reversal, with prices declining to $2,610 on Monday after recent highs. This downward movement follows a temporary rally post-U.S. election, but gold was unable to sustain a price above $2,700. With prices now below the 50-day simple moving average (SMA), a technical break below $2,600 could signal further declines.

XAU/USD – H4 Chart

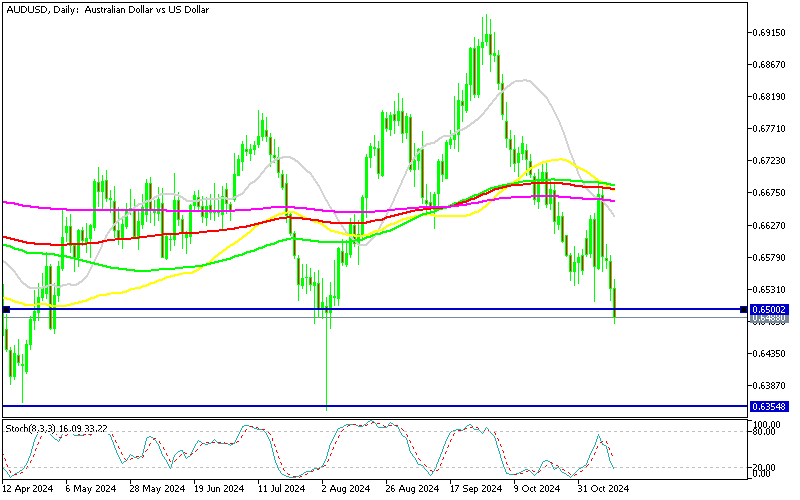

AUD/USD Breaks Below 0.65

The AUD/USD also experienced notable movement, falling 4 cents in October. Sellers maintained control due to a combination of technical indicators and economic factors, with a brief rally last week on hopes of Chinese stimulus quickly fading. The pair dropped back down to the key support level of 0.65 as daily moving averages held, making a further breach of this level increasingly likely.

AUD/USD – Daily Chart

Cryptocurrency Update

The Surge in Bitcoin Doesn’t Seem to End

BTC/USD – Daily chart

Ethereum Pushes Above $3,000

Ethereum has also displayed bullish momentum, breaking above its 100-day SMA and attracting significant buying interest. After dipping below $2,500, Ethereum regained support, crossed the 50-day SMA, and surged past $3,000 over the weekend. Yesterday, ETH/USD continued its climb to $3,450 before seeing a pullback. Both Bitcoin and Ethereum are reflecting investor optimism but remain subject to market corrections.

ETH/USD – Daily chart